Stablecoin Taxonomy & Money Supply (Part II)

- Apr 3

- 25 min read

Updated: Apr 4

This is a continuation of Part I.

Table of Contents

Part II: Stablecoin Money Supply

Stablecoin Money Supply

3.1. Overview

3.2. Monetary Aggregates

3.3. Stablecoin M0 & M1

3.4. Liquidity & Stability

3.5. Stablecoin M2 & M3

3.6. Supply Contraction

3.7. Re-Lending & Recursive Lending

3.8. Meta-Money Supply

3.9. Fiat vs. CDPS vs. RBS

3.10. Money Supply Comparison

Conclusion

References

Stablecoin Money Supply

3.1. Overview

In modern banking, both money and loans are created endogenously together under a credit creation → deposit liabilities → reserve settlement model, i.e., fractional-reserve banking. By contrast, RBS operate on an exogenous monetary base that is full-reserve, where token issuance and credit formation take place separately under a reserve settlement → token liabilities → credit intermediation model.

Traditionally, fiat credit expansion increases the total money supply, while credit contraction decreases it. However, credit expansion for an RBS can actually reduce its token supply, while credit contraction may re-grow it. These RBS dynamics are structurally inverted vs. fiat due to the separation between money and credit in a full-reserve system.

a. Fiat Credit Creation Process

Endogenous bank lending → Money creation → Deposits & spending → Interbank reserve settlements & central bank accommodation → More lending & spending → Money supply expansion.

Commercial banks “print” new loans endogenously, which are recorded as bank assets. Loans simultaneously create new money as bank deposit liabilities, expanding the total money supply.

Borrowers spend the newly created deposits, circulating bank money into the economy. Most of it is re-deposited back into commercial banks.

As deposits move between banks, interbank payments are settled using reserves, which shift between their master accounts at the central bank to clear net payment flows.

The central bank accommodates reserve demand as needed, supplying commercial banks with base money elastically through bank asset (loan) purchases, lending facilities, and other balance sheet tools to maintain its policy targets.

As long as reserve settlements function smoothly, commercial banks can continue extending loans, further raising deposits and spending activity. This allows credit and deposit balances to expand the total money supply. If credit and money creation outpace real economic productivity, it may result in inflation and systemic instability.

b. RBS Credit Intermediation Process

Exogenous reserves → Stablecoin issuance → Lending deposits → Borrowing & spending → Arbitrage & redemptions (if market liquidity is low) → Reserve outflows → Token supply contraction.

The stablecoin issuer creates new tokens as liabilities only when minters have deposited reserve assets. These assets fully back the stablecoin supply on a 1:1 basis, enforcing a hard peg via direct redemption.

Users receive newly minted stablecoins in their wallets. Unlike bank money, RBS cannot be created from loans. Therefore, the stablecoin’s circulating supply should never exceed the size of its underlying reserve.

Users can now transfer stablecoins between wallets, exchanges, and decentralized applications, settling them directly on blockchain networks.

For borrowers to access credit, lenders must first deposit stablecoins into lending markets after minting them. Once borrowed, the stablecoins are sold or redeemed if market liquidity cannot absorb selling pressures sufficiently. This contracts circulating supply and underlying reserves as debt increases in the system.

Reserves act as an explicit backstop to support peg stability and limit credit expansion. Until new reserves, deposits, or liquidity enter the system, new loans cannot be intermediated.

3.2. Monetary Aggregates

Central banks have yet to determine how to formally incorporate stablecoins, particularly regulated payment stablecoins (RBS), into existing monetary aggregates such as M0, M1, M2, and M3. Since a large share of stablecoin reserves currently consist of government securities, they could be viewed as tokenized claims on sovereign credit (without embedded yield for token holders). However, from a transactional perspective, payment stablecoins still function similarly to digital cash. This hybrid nature complicates their classification within traditional aggregates, raising the question of whether stablecoins should be treated as narrow money, near money, or broad money. The answer will materially affect how central bankers, policymakers, and regulators treat stablecoins in the long run.

When analyzed as a standalone monetary system, an RBS’s money supply can be measured using aggregate classifications analogous to those used in fiat systems:

3.3. Stablecoin M0 & M1

External reserve assets form an RBS’s monetary base (M0), providing final settlement liquidity while backing the circulating supply (M1) on a 1:1 basis at minimum.

M1 includes all stablecoins in circulation in user wallets, exchanges, bridges, and smart contracts that are immediately redeemable or transferable, and are not rehypothecated. This is considered the stablecoin’s narrow money supply.

Unlike fiat money which has an endogenous monetary base, an RBS’s monetary base is exogenous and non-fungible with the token itself. As a result, M1 does not include M0 within its definition for these stablecoins.

Unlike bank money (deposit liabilities), RBS (token liabilities) must be collateralized 1:1, which means their M1 should not be greater than M0.

3.4. Liquidity & Stability

A stablecoin cannot sustain meaningful secondary market price discovery unless it is liquid or tradable. The aggregate value of all other assets actively paired against the stablecoin on exchanges is what enables secondary market liquidity for it.

Market price is based on aggregate liquidity paired against the stablecoin’s tradable supply, where marginal order flows determine prevailing exchange rates between it and other assets. More stablecoins vs. paired liquidity = downward peg pressure; fewer stablecoins vs. paired liquidity = upward peg pressure.

As long as there is 1:1 redemption and confidence in the issuer, market makers will naturally arbitrage the stablecoin to maintain its liquidity balance and peg stability. If there is low arbitrage activity, the issuer could intervene directly through open market operations instead of waiting for market makers to perform arbitrage.

Strong secondary market liquidity enables larger capital entry/exit, reducing peg deviation and slippage while improving money elasticity and velocity for the stablecoin across market cycles.

3.5. Stablecoin M2 & M3

Today, most lending protocols operate onchain money markets that offer short-term, revolving credit (e.g., Aave). Stablecoins are commonly supplied into these markets, where borrowers can take out loans and pay interest to lenders. However, lenders can only withdraw stablecoins that are idle. Borrowed stablecoins (deposit liabilities) must be repaid before lenders can withdraw.

Stablecoin money market interest rate models in DeFi are typically determined by demand (debt) relative to supply (deposits), or credit utilization (debt ÷ deposits). Higher utilization = higher rates; lower utilization = lower rates.

When utilization rises and withdrawals become constrained, interest rates increase dynamically, incentivizing borrowers to repay. This self-balancing mechanism eventually restores liquidity and enables lender withdrawals.

To ensure lender solvency, stablecoin loans in DeFi are usually over-collateralized by assets from borrowers. When a borrower’s position reaches a pre-specified liquidation threshold, their collateral is quickly sold to repay debt and restore liquidity for lenders.

Debts in money markets increase the stablecoin’s near money supply (M2) and broad money supply (M3), which consists of stablecoins in circulation, including idle deposits in lending markets plus less liquid deposits that are actively lent out but not immediately withdrawable until borrowers repay.

M2 and M3 both include M1 within their definition because lent deposits are still claims on the stablecoin’s supply, whether it is still circulating or has been redeemed/removed from circulation.

Traditional near money instruments typically mature in <2 years, but stablecoin money market deposits do not have fixed maturity dates because they operate as open-ended revolving credit facilities. However, their loan durations tend to be short due to frequent borrower repayments. On Aave, 56% of loans have durations of <30 days.

Deposits are rarely lent out 100% since interest rates rise sharply at high utilization. When this happens, borrowers are naturally incentivized to reduce debt. As a result, a portion of deposits typically remains idle and available for immediate withdrawal, allowing stablecoin money markets in DeFi to behave like near money.

![Figure 15. Aave loan duration statistics. Source: Dune, as of December 2025. [8]](https://static.wixstatic.com/media/a1dd13_9b5893a72c154bf2bd50abec37299897~mv2.png/v1/fill/w_821,h_322,al_c,q_85,enc_avif,quality_auto/a1dd13_9b5893a72c154bf2bd50abec37299897~mv2.png)

Small stablecoin deposit liabilities with <$100K and <2 years maturity are considered part of the stablecoin’s M2 supply, which includes M1 plus money market and term deposits in CeFi/DeFi as well as staked or locked tokens in general across wallets and smart contracts.

Large stablecoin deposit liabilities with >$100K and <2 years maturity are considered part of the stablecoin’s M3 supply, which includes M2 plus similar but larger liabilities that may be less liquid than near money.

3.6. Supply Contraction

When an RBS is borrowed, it may end up getting redeemed, either directly by borrowers or indirectly by market makers who bought it from borrowers. As a result, credit expansion ultimately can contract the stablecoin’s M0/M1 supply when there is insufficient secondary market liquidity to fully absorb selling pressures from borrowers.

Eventually, when borrowers de-leverage, they have to buy back or mint new stablecoins to repay their debt. This naturally reintroduces base reserves and circulating supply back into the system. Thus, credit contraction re-expands the stablecoin’s M0/M1 supply.

When sufficient secondary market liquidity exists, credit expansion may not contract M0/M1. Paired liquidity for the stablecoin can expand on exchanges, allowing market makers and liquidity providers to absorb selling from borrowers and reduce redemption pressures.

Credit velocity (borrows + repays) increases the token’s trading volume and money velocity as borrowers sell stablecoins to leverage, then buy them back later to unwind debt and de-leverage. This generates potential earnings for market makers and liquidity providers over time through trading fees and/or arbitrage profits.

The existence of many trading venues and liquidity pools for the stablecoin increases cross-market arbitrage opportunities for market makers and liquidity providers. This further enhances potential trading profits, incentivizing additional liquidity while supporting stronger price stability over time.

If market makers and liquidity providers earn sufficient returns, they are incentivized to keep capital deployed. The presence of additional secondary market liquidity from these participants may add net growth to the stablecoin’s total money supply, even during credit expansion cycles.

In the complete absence of secondary market liquidity, each unit of debt eventually contracts an equivalent unit of M0/M1 as borrowers must redeem stablecoins to access final settlement liquidity. With the existence of secondary market liquidity, each unit of debt decreases less than one unit of M0/M1.

When an RBS is used as backing for another stablecoin or digital asset with its own credit activity, downstream credit expansion of the new asset may introduce additional redemption pressure on the base RBS reserves. This could potentially compound with redemption flows from the RBS’s native credit activity, amplifying reserve outflows and further contracting M0/M1.

When an RBS’s lending deposits are used as backing for another stablecoin or digital asset with its own credit activity, downstream credit expansion of the new asset may force upstream credit contraction, as withdrawals and redemptions propagate back through the stack. This dynamic can simultaneously reduce both base RBS reserves and total money supply.

3.7. Re-Lending & Recursive Lending

Users may re-lend borrowed stablecoins in the short term for various reasons, such as “farming” DeFi incentives, or keeping idle liquidity productive and relatively mobile. Credit expansion from borrower-driven re-lending does not immediately create selling or redemption pressures, allowing M2/M3 to expand without contracting M0/M1.

If users borrow a stablecoin against itself as collateral to re-lend, often in the short term, it is considered recursive lending, where both re-lending and rehypothecation are involved. Recursive lending also expands M2/M3 without immediately contracting M0/M1.

If lenders acquire tokens previously sold by borrowers on exchanges and resupply them into lending protocols, it is considered lender-driven re-lending. When these tokens are bought and re-lent, additional credit and M2/M3 deposit liabilities can be created without requiring M0/M1 to expand in parallel.

Re-lending and recursive lending enable M3 to exceed M1 prior to borrower and arbitrageur- driven redemption outflows, creating layered credit claims on the same number of stablecoins in circulation. Without re-lending and recursive lending, the maximum theoretical credit expansion capacity (M3 - M1) is capped at 100% of M1 supply in lending deposits prior to redemptionary contraction. With re-lending and recursive lending, effective credit expansion may exceed it.

Ultimately, re-lent deposits are borrowed by users who need settlement liquidity, which can lead to M0/M1 contraction due to redemptions. However, they must eventually buy back or mint new tokens to repay debt, allowing M0/M1 to re-expand during credit contraction cycles.

Borrower-driven re-lending and recursive lending don’t typically create net growth in the stablecoin’s M0/M1 supply during credit contraction cycles because borrowers can simply repay debt with the same deposits they are already holding, as long as those tokens were not borrowed and redeemed out of the system.

On the other hand, lender-driven re-lending transforms debt repayments into new base reserves and circulating supply during credit contraction cycles because repayment requires borrowers to buy back or mint new tokens, thereby re-expanding M0/M1 rather than merely netting out existing deposit liabilities. If lenders continue deploying capital after borrowers have de-leveraged, re-lending can result in net M0/M1 growth over the full credit cycle.

3.8. Meta-Money Supply

a. DeFi Composability

In DeFi, composability allows tokens and protocols to be combined permissionlessly as modular financial primitives, or “money legos,” synthesizing new products and applications that may unlock additional capital efficiency, yield, and liquidity. However, this interconnectivity also increases systemic risk as failures in one layer can quickly propagate across dependent systems.

To enable composability, many DeFi protocols produce receipt tokens or derivative tokens to function as redeemable shares of user deposits. For example:

Cross-chain bridges mint wrapped or bridged tokens representing claims on tokens such as stablecoins that are locked on another blockchain. The bridged token enables a derivative of the stablecoin to circulate on the destination chain while maintaining redeemability for the underlying asset held in bridge custody.

Stablecoin liquidity pools in DEXs produce LP tokens. The LP token represents a claim on one unit of liquidity, composed of the stablecoin and another paired asset(s). Liquidity providers can redeem the LP token to withdraw either asset that is available in the pool. LP tokens can also be staked into “yield farming” protocols to gain additional rewards or boost their earnings against other unstaked tokens.

ERC-4626 vaults can tokenize stablecoin deposits in onchain money markets, allowing lenders to mint lending-based yieldcoins. The yieldcoin represents a claim on one unit of lending supply. It is effectively backed by both utilized credit and idle stablecoins in the lending protocol, where loans are secured by collateral from borrowers. Holders can redeem the yieldcoin for underlying stablecoins in these money markets, subject to available liquidity. Holders can also supply yieldcoins into lending protocols as collateral to borrow stablecoins, where the underlying yields offset interest expenses and enable lower net borrowing costs. They may even engage in yield “looping” (leveraged carry trading) strategies to amplify potential returns if the stablecoin’s borrowing rate is lower than the yieldcoin’s native rate.

Some protocols issue second-order stablecoins that are backed by other stablecoins and/or yieldcoins. The new token represents a claim on other token liabilities or deposit liabilities rather than a direct claim on their underlying reserves, introducing an additional layer of abstraction.

Receipt tokens and yieldcoins can be supplied into other DeFi protocols to create additional layers of derivatives. For example, yieldcoins can be supplied as collateral and liquidity in Pendle, the world’s largest decentralized interest rate marketplace, to enable yield speculation or hedging via PTs (principal tokens) and YTs (yield tokens).

PTs represent the principal value of the underlying yieldcoin at maturity. PT holders forgo interim yield but can redeem the full notional value of the asset at expiration, making PTs economically similar to zero-coupon bonds.

YTs represent the future yield generated by the underlying yieldcoin during the specified maturity period. YT holders receive all yield produced by the asset until expiration, allowing traders to speculate on or gain leveraged exposure to changes in yield rates.

ℹ️ Note: Yieldcoins typically carry a single-asset denomination tied directly to one stablecoin and its deposit liabilities, whereas LP tokens are multi-asset claims on DEX deposits that are redeemable for either a stablecoin or another paired asset(s), subject to available liquidity.

![Figure 20. Composable DeFi strategy examples. Source: Artemis Analytics & Vaults.fyi. [9]](https://static.wixstatic.com/media/a1dd13_cc8fe275a40840629fb8e1cf9274aa1a~mv2.png/v1/fill/w_975,h_1163,al_c,q_90,enc_avif,quality_auto/a1dd13_cc8fe275a40840629fb8e1cf9274aa1a~mv2.png)

b. Layered Liabilities

Just as M0 constitutes an RBS’s monetary base, its M1/M2/M3 money supply collectively forms the meta-monetary base (MM0) of higher-order token liabilities.

Receipt tokens form the meta-narrow money supply (MM1) of an RBS. MM1 represents tokenized M1/M2/M3 claims that are directly redeemable for underlying tokens or deposit liabilities, subject to available liquidity. Credit markets for MM1 tokens may also emerge, creating higher-order deposit liabilities that form their meta-near and meta-broad money supply (MM2/MM3), similar to M2/M3.

However, for MM1 assets to function as a high-velocity medium of exchange or credit, they need to be non-yield-bearing. Because many receipts (excluding non-rehypothecated bridged tokens) auto-embed yield, they are more likely to be used as collateral for borrowing, exchange liquidity, or simply for savings—not as lending liquidity, since borrowers typically avoid loans denominated in yield-bearing assets.

To enable credit activity, some DeFi protocols “wrap” or tokenize yield-bearing MM1 assets from external systems into second-order stablecoins that do not embed yield, transforming the original MM1 assets into a new M0² monetary base that supports a distinct M1² token liability structure. The underlying yield (float income) can then be redistributed into M2² or M3² deposits associated with the M1² stablecoin. Additionally, M2²/M3² deposits may themselves issue receipt tokens, forming an MM1² layer that can function as M0³ base reserves for M1³ RBS with their own M2³/M3³ credit layers. This recursive structure may continue in other layers, creating increasingly abstracted monetary hierarchies within DeFi.

Although RBS operate under a full-reserve, narrow banking-like framework with limited native capacity for credit expansion compared to fractional-reserve banking, onchain composability can reintroduce leverage via layered financial engineering. Through receipt tokens, onchain derivatives, rehypothecation, and recursive wrapping across protocols, DeFi infrastructure allows secondary and higher-order credit claims to emerge on top of fully reserved base assets. This allows effective credit supply in the system to expand significantly beyond the original RBS monetary base, producing leverage dynamics that may functionally resemble fractional-reserve systems.

c. Systemic Risk

Naturally, these additional layers of financial engineering introduce significant structural complexity, leverage, and systemic risk. Because DeFi is composable, interoperable, and permissionless, instability in the meta layers can rapidly propagate downward, especially if receipt and derivative tokens are used recursively as reserves or collateral for new liabilities.

Additionally, the coexistence of multiple stablecoins with different issuers, reserve structures, liquidity conditions, and redemption mechanisms—combined with composability across protocols, bridges, and derivatives—can weaken the effective singleness of money observed in traditional fiat systems, where different forms of money (bank deposits, reserves, cash) remain fungible and interchangeable at par within a unified monetary hierarchy. In contrast, DeFi ecosystems contain numerous stablecoins with heterogeneous risk profiles, liquidity, and market structures. As these assets interact with composable protocols, fragmentation can emerge in what would traditionally function as a single monetary unit.

The scale of systemic and contagion risks from inter-protocol dependencies has been repeatedly documented throughout DeFi’s history, where impacts from incidents in higher-order layers quickly spread into lower-order ecosystems. For example:

USTC, Terra’s classic algorithmic stablecoin, depended heavily on reflexive arbitrage incentives and secondary market liquidity on exchanges to maintain peg stability. When confidence collapsed in May 2022, liquidity withdrawals drained USTC pools and accelerated its collapse. While USTC was not backed by other stablecoins, it was paired extensively with them in liquidity pools. This resulted in stress throughout the market, contributing to a temporary de-peg of USDT during the crisis. Numerous other protocols, funds, and leveraged strategies that integrated with the Terra ecosystem also unraveled, resulting in around $50 billion of combined market value getting wiped out within days. [10]

Stream Finance was a yieldcoin protocol that issued xUSD, a structured yieldcoin layered on top of underlying stablecoin liquidity and leveraged strategies. In November 2025, xUSD collapsed following revelations of $93 million in losses. The disclosure triggered a rapid loss of confidence, freezing of protocol activity, depegging of xUSD, and cascading liquidations across DeFi. The contagion was particularly severe on chains where xUSD held significant market share, leading to roughly $285 million in user losses from ecosystem failures, including second-order assets that were directly exposed and third-order protocols with indirect exposure to xUSD. [11]

As composability and interoperability continue to deepen in DeFi, future stress events may exert direct redemption, liquidity, or confidence pressures on foundational stablecoin systems in ways not yet observed at scale. Because higher-order claims and receipt tokens are often layered recursively among protocols, instability at one level can transmit quickly throughout interconnected systems. Risk managers therefore need to analyze both the core monetary aggregates and the broader meta-money supply to properly assess risk exposures within integrated ecosystems.

Lastly, because the meta-money supply represents secondary and higher-order claims layered on top of lower-order token/deposit liabilities, it should not be incorporated into core stablecoin monetary aggregates, which only consist of primary token and deposit liabilities. Nonetheless, it carries major macroeconomic significance, as the meta-money supply of a stablecoin can materially influence monetary conditions as well as systemic dynamics in the onchain economy and, gradually, the real-world economy.

3.9. Fiat vs. RBS vs. CDPS

While both RBS and CDPS may appear similar at a high level, their monetary structures, credit mechanisms, and systemic dynamics differ fundamentally. These differences influence how each system expands credit, maintains peg stability, and interacts with broader financial markets.

a. Credit Mechanisms

The fundamental distinction between CDPS and RBS systems lies in how new money enters circulation and how credit arises within the monetary system.

Pure CDPS create new money (tokens) through debt issuance. When users open a CDP, the protocol mints new stablecoins while recording a corresponding debt obligation. Borrowers must eventually repay the debt along with interest or “stability fees.” As a result, CDPS create credit directly at the primary issuance layer, enabling credit expansion without requiring pre-funded lending deposits.

RBS, by contrast, do not create new money through debt. Because tokens are issued only against reserves on a 1:1 basis, issuance carries no inherent credit cost and does not generate credit at the primary layer. Credit intermediation instead arises in secondary lending markets through pre-funded lending deposits.

Notably, CDPS are structurally similar to the modern fiat banking system in that both operate as endogenous money and credit creation mechanisms.

In fiat banking, deposits are created when banks extend loans. The newly created deposits are then used by borrowers to purchase assets such as houses, which subsequently function as collateral for the loan.

CDPS operate under a similar structure, except that collateral must be posted before credit is created. In this case, borrowers deposit collateral into a smart contract, after which the protocol mints new stablecoins against that collateral.

The key distinction between fiat and CDPS therefore lies in the timing of collateralization in credit creation. In fiat banking, credit is ex-post collateralized, meaning loans create deposits first and collateral relationships form afterward, whereas CDPS are ex-ante collateralized, requiring collateral to be posted before new credit/stablecoins can be issued.

b. Fiat Monetary Structure

Modern fractional-reserve banking is often misunderstood as a system where banks strictly lend out a portion of customer deposits. In practice, however, commercial banks today create new deposit liabilities when they extend loans endogenously, without necessarily re-lending customer deposits.

When a bank issues a loan, a corresponding deposit is simultaneously created on the bank’s balance sheet as a liability, making depositors unsecured creditors of the bank. These deposits expand the money supply even though they are not funded by prior deposits, allowing banks to expand M1 independently of their reserve balances held at the central bank. However, banks must maintain sufficient reserves to settle payments with other banks, which they can obtain through interbank markets or from the central bank.

When customers transfer deposits between banks, the sending bank must settle reserves with the receiving bank through central bank settlement systems. If deposit outflows exceed reserve inflows, the bank may experience reserve shortages and liquidity stress. Under normal conditions, reserve flows in the banking system usually balance out as banks continuously receive deposits from other institutions. During periods of stress, banks may sell assets to the central bank or borrow reserves using those assets as collateral.

Central banks can also expand reserves by purchasing assets or lending against collateral, injecting liquidity into the system to stabilize financial markets at the potential cost of inflation and currency devaluation (i.e., socialized losses) if credit outpaces real economic productivity.

Under this structure, bank deposits effectively function as lending deposits because they originate from credit creation within the banking system, even though they may not be re-lent by the bank.

Fiat monetary aggregates (Fed definitions):

M0 = Endogenous reserves + physical cash

M1 = M0 + liquid bank deposits (checking, savings, MMAs)

M2/M3 = M1 + near-liquid bank deposits, MMFs, repos, eurodollars, other large assets

Example of fiat balance sheet structure with credit creation and contraction:

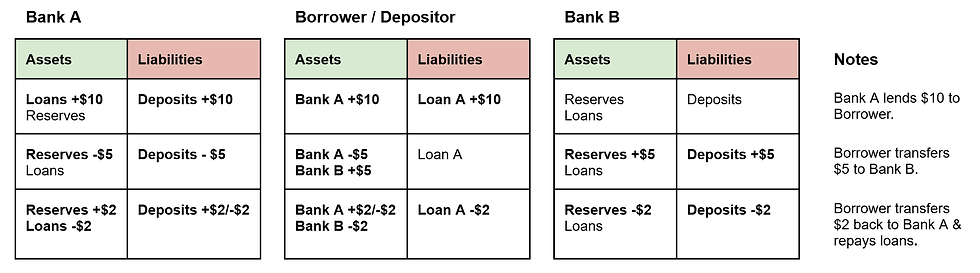

c. RBS Monetary Structure

RBS operate more similarly to narrow banking systems, where both money creation and credit expansion are constrained by reserve backing.

Unlike fiat banking, where M1 can significantly exceed M0, RBS requires reserves to match token liabilities on a 1:1 basis (at least 100%). Because of this structure, new credit cannot be created through stablecoin issuance itself. Lending activity associated with RBS therefore appears only in M2/M3 layers through pre-funded CeFi/DeFi lending deposits. Additionally, RBS credit expansion is also limited by the size of its M0 reserves, M1 liquidity pools, plus M2/M3 lending deposits.

In fiat banking models, the money supply multiplier is commonly approximated as 1 ÷ reserve ratio. The reserve ratio is the fraction of deposits commercial banks must legally hold as reserves (base money). Because banks can still re-lend the remaining portion, credit expansion creates new deposit liabilities and progressively increases the total money supply. In practice, however, modern banks today create loans endogenously and acquire reserves later to settle interbank payments.

For example, with a 10% reserve ratio, $1 of base money may support $9 of additional deposits/loans, resulting in $10 of total money supply, or a 10x multiplier.

In RBS systems, the money multiplier is similarly constrained by the average idle deposit ratio across lending markets, approximated as 1 ÷ idle ratio. Additionally, credit expansion in an RBS causes its money multiplier to increase regressively because borrowed stablecoins are typically redeemed for underlying reserves, contracting M0/M1 if there is insufficient secondary market liquidity to divert redemption pressures.

For example, let’s hypothetically assume a 10% idle ratio and zero market liquidity support for USDT. 9 USDT are then borrowed and redeemed out of 10 USDT in lending deposits, leaving only 1 idle USDT in circulation. The total money supply here is 10 USDT—also a 10x multiplier, but with a 90% contraction in circulating supply.

The idle ratio is largely determined by the cost of credit, especially in lending protocols with dynamic interest rate models, where rates rise sharply once utilization exceeds optimal levels to discourage excessive borrowing. As a result, the average idle ratio tends to anchor around optimal utilization levels across lending protocols.

RBS monetary aggregates:

M0 = Exogenous reserve backing

M1 = Circulating stablecoins in wallets + deposits that are liquid and not rehypothecated

M2/M3 = M1 + stablecoin lending deposits with <2 years maturity

Example of RBS balance sheet structure with credit intermediation, expansion, and contraction:

ℹ️ Note: SBS follow a similar structure to RBS because tokens are created against deposited capital rather than endogenous debt. However, while RBS are backed by relatively static reserve assets, SBS rely on actively managed or programmatic strategies. As a result, the backing and risk profile of SBS depend on additional factors such as the underlying strategy’s performance, solvency, and liquidity.

d. CDPS Monetary Structure

Pure CDPS operate under a different monetary architecture because they do not have a reserve layer.

CDPS loans are originated within the token supply itself when borrowers mint new token liabilities through collateralized debt positions. As a result, CDPS effectively begin at the M1 layer just like in fiat systems, where tokens enter circulation post-credit creation. While credit intermediation can also take place via secondary lending markets, primary credit creation already occurs within M1.

CDPS do not have an M0 layer because locked collateral is not directly redeemable by stablecoin holders, preventing it from functioning as final settlement liquidity. Instead, collateral securing debt positions can only be withdrawn after loans are repaid, thereby contracting credit and M1. Meanwhile, RBS operate in the opposite direction: credit contraction increases M0/M1 while credit expansion reduces M0/M1 (in the absence of market liquidity support).

In theory, a CDPS’s credit capacity is constrained by its collateralization requirements. In practice, however, the main limiting factor tends to be secondary market liquidity, which must absorb most of the CDPS borrowers’ sell orders. This dynamic often contributes to peg instability in new CDPS projects. If the soft peg trades at a significant discount due to low market liquidity, CDPS borrowers effectively incur a higher cost of credit, as they receive less value from selling the stablecoin even if nominal borrowing rates remain low.

CDPS therefore require deep secondary market liquidity to enable effective credit expansion without causing significant de-pegs. RBS, on the other hand, do not need secondary market liquidity to enable credit expansion because borrowers can always redeem stablecoins to access underlying reserve liquidity directly.

Liquidity providers for CDPS are effectively ex-post lenders who supply secondary market liquidity to support credit after it has already been created at the primary issuance layer.

CDPS monetary aggregates:

M1 = Circulating stablecoins in wallets + deposits that are liquid and not rehypothecated

M2/M3 = M1 + stablecoin deposits with <2 years maturity

CDPS examples:

Liquity (BOLD) operates as a pure ex-ante, endogenous CDP stablecoin system, where stablecoins are minted directly from collateralized debt positions without a reserve layer.

Sky (USDS) operates as a hybrid stablecoin system with ex-ante, endogenous CDPs + exogenous reserves, resulting in a mixed monetary structure.

Example of CDPS balance sheet structure with credit creation and contraction:

3.10. Money Supply Comparison

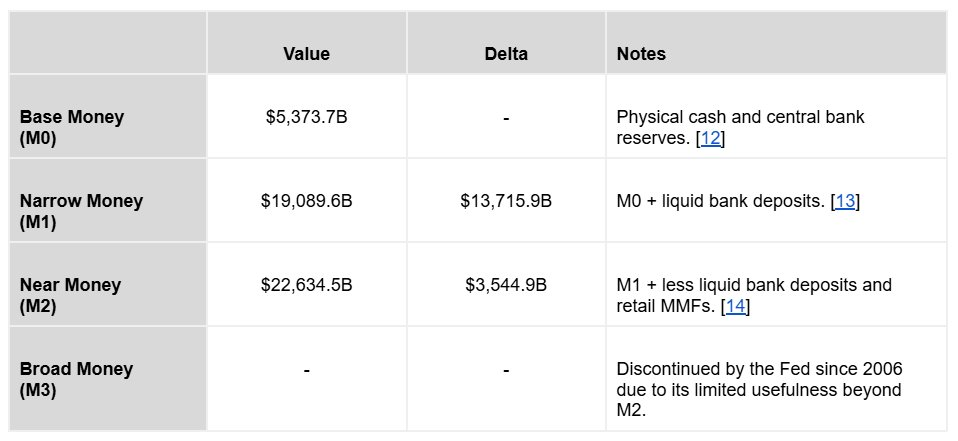

a. U.S. Dollar

As of December 2025, FRED reported the following statistics for USD monetary aggregates:

The M2 multiplier (M2 ÷ M0) for USD is about 4.21x, meaning every $1 of base money creates about $3.21 of additional bank deposits. This reflects the banking system’s ability to expand the money supply through credit creation, allowing base money to support a much larger stock of commercial bank liabilities.

In May 2020, the Fed removed the six-transfer limit on savings deposits under Regulation D. As a result, savings deposits, including MMAs, were reclassified from M2 into M1. This one-time change increased reported M1 by roughly $11.2 trillion but did not represent a true expansion of the underlying money supply.

b. Stablecoins

As of the end of 2025, industry sources reported the following statistics for USDT, USDC, USDS, and DAI, the world’s largest stablecoins with close to 90% in combined market share:

Total M3 supply for these stablecoins is about $307.5 billion vs. $272.3 billion in combined M1, implying a ~1.13x multiplier (M3 ÷ M1). This is nearly four times lower than the M2 multiplier for USD, reflecting the low-leverage, narrow banking-like limits of RBS systems, where credit must be supported by pre-funded lending deposits.

~$1.6 billion of M1 originated from Sky’s CDP positions. This means less than 1% of stablecoin supply emerged from credit creation, while the rest came from reserve-backed issuance.

CeFi is the leading channel for stablecoin-denominated credit intermediation, where active debt is ~60% larger than in DeFi. Tether alone accounts for ~61% of CeFi loans across all assets. [18] Additionally, USDT dominates ~70% of all active stablecoin loans in CeFi/DeFi.

The majority of stablecoin supply remains idle for lending activity. While combined M3 is $307.5 billion, outstanding stablecoin debt across CeFi/DeFi is estimated at around $35.1 billion, which means only ~11.4% of stablecoin broad money supply is involved in credit intermediation.

By contrast, the fiat banking system creates and intermediates credit far more extensively, with about $17.3 trillion of M2 deposits and money market instruments layered on top of $5.4 trillion of M0. This means 76.7% of the USD money stock exists beyond the monetary base.

Stablecoin-denominated credit, however, is still extremely small in absolute terms, accounting for less than 0.1% of the $45 trillion global credit market. [22] As adoption continues to accelerate, credit supply and utilization are expected to increase in stablecoin lending markets, organically raising their aggregate M3 multiplier in the future.

Conclusion

Stablecoins are evolving beyond simple fiat-backed designs, and accurate classification must shift from an academic exercise to a prerequisite for effective economic implementation and risk management. A more precise taxonomy allows for clearer differentiation between stablecoin designs, especially as newer unregulated models increasingly blend elements of RBS, SBS, CDPS, and endogenous systems. Without this clarity, risks may be mispriced, dependencies underestimated, and market behavior misinterpreted.

A key structural insight is that RBS operate under a monetary dynamic that is inverse to fiat systems. In a full-reserve framework, credit expansion can reduce base reserves and circulating supply through redemption flows, rather than expand total money supply like in fractional-reserve banking. However, this constraint is not absolute. Through composability, secondary lending, and layered claims on base assets, DeFi reintroduces leverage at scale via the meta-money supply. These higher-order structures may improve capital efficiency, but they also create additional channels for liquidity stress and systemic risk that extend beyond the base system.

At present, stablecoin money multipliers are significantly lower than in fiat money. While this partly reflects the narrow banking-like constraints of full-reserve issuance, a more immediate driver is the relative immaturity of stablecoin credit markets. As a result, a large share of global stablecoin supply remains idle, limiting the depth and scale of credit formation. With continued maturation and growing utilization, these multipliers will likely increase, introducing more complex credit dynamics into the system.

As stablecoins expand to more financial use cases, it becomes increasingly important to assess them not as a single asset class, but as a heterogeneous set of monetary systems with distinct properties, risks, and market dynamics. How these dynamics ultimately evolve is hard to predict, given the rapid pace of innovation in the onchain economy, including the emergence of yieldcoins and agentic applications. A disciplined taxonomy, combined with rigorous analyses of both core and meta-monetary aggregates, can support clearer interpretations and more effective stablecoin designs, risk management, and regulations.

References

[8] Dune Analytics (@walledao), Aave vs Spark: Deep Dive into DeFi Lending.

[9] Artemis Analytics & Vaults.fyi, Onchain Yields: What the Data Shows & What’s Next.

[10] Federal Reserve Board, Interconnected DeFi: Ripple Effects from the Terra Collapse.

[11] BlockEden, Anatomy of a $285M DeFi Contagion: The Stream Finance xUSD Collapse.

[12] Federal Reserve Bank of St. Louis (FRED), Monetary Base: Total (BOGMBASE).

[13] Federal Reserve Bank of St. Louis (FRED), M1 Money Stock (M1SL).

[14] Federal Reserve Bank of St. Louis (FRED), M2 Money Stock (M2SL).

[15] Tether, Transparency Report.

[16] Circle, Transparency Report.

[17] Sky & Block Analitica, Sky Ecosystem Collateral Dashboard.

[18] Galaxy Research, The State of Crypto Leverage: Q4 2025 – Surviving a Stress Test.

[19] OpenAI, ChatGPT 5.3 – Custom Research Output (internal tool).

[20] DefiLlama, LlamaAI – Custom Research Output (internal tool).

[21] DefiLlama, LlamaAI – Custom Research Output (internal tool).

[22] KKR, The Power of Credit.

About Us

Stably is a stablecoin technology and advisory firm from Seattle, Washington. The company specializes in infrastructure development and strategic consulting for stablecoin issuers, financial institutions, and DeFi protocols. Stably issued the world’s fifth USD-backed stablecoin in 2018, pioneered Stablecoin-as-a-Service (SCaaS) in 2019, powered one of the first gold-backed tokens in 2021, and developed the first decentralized stablecoin with interest rebates in 2024. Since inception, Stably has supported over 20 stablecoin launches with battle-tested infrastructure and 8+ years of industry experience. Learn more at stably.io

Contributors

Kory Hoang | Co-founder, CEO Background: 10+ years of financial industry experience, with prior backgrounds at PitchBook & Bank of America. Kory leads strategy, operation, advisory & stablecoinomics at Stably.

David Zhang | Co-founder, CTO Background: 10+ years of tech & product experience, with a previous background at Amazon. David leads engineering, AI integrations, product development, risk management & security at Stably.

Disclaimer

This document is provided solely for informational and educational purposes and does not constitute financial, investment, legal, tax, accounting, regulatory, or other professional advice. Nothing contained herein should be interpreted as a recommendation, solicitation, or endorsement to buy, sell, issue, hold, or transact in any digital asset, stablecoin, yieldcoin, security, derivative instrument, or financial product.

The material presented in this document reflects the authors’ views, interpretations, and analytical frameworks regarding stablecoins, decentralized finance (DeFi), digital monetary systems, and related financial infrastructure. These views may evolve over time and may differ from those held by regulators, financial institutions, academic researchers, or other market participants. Certain frameworks, terminology, and taxonomies described herein may represent conceptual interpretations or emerging industry perspectives that are not yet formally recognized or standardized within regulatory, academic, or financial literature.

This document may contain forward-looking statements, projections, or hypothetical scenarios regarding financial systems, blockchain networks, or digital asset markets. Such statements involve known and unknown risks, uncertainties, and assumptions, and actual outcomes may differ materially from those described. No representation or warranty is made regarding the completeness, accuracy, reliability, or timeliness of any information contained in this document.

Digital assets, including stablecoins and yieldcoins, involve significant risks, including but not limited to market volatility, liquidity risk, credit risk, counterparty risk, smart contract vulnerabilities, cybersecurity threats, operational failures, regulatory changes, and potential loss of funds. Stablecoins may de-peg or lose value, and digital assets are generally not insured by governments, central banks, or deposit insurance schemes. Participation in blockchain networks, DeFi protocols, or digital asset markets may expose users to technical, financial, and legal risks that may not be fully understood.

The information contained herein is derived from publicly available sources, industry data, protocol documentation, and analytical interpretations believed to be reliable at the time of publication. However, the authors and publishers do not guarantee the accuracy or completeness of such information and assume no obligation to update or correct it as circumstances change.

Nothing in this document should be interpreted as an offer to issue or purchase securities, stablecoins, yieldcoins, cryptocurrencies, or other digital assets, nor as a representation regarding the regulatory status of any token, protocol, or financial structure described herein. Regulatory treatment of digital assets varies by jurisdiction and continues to evolve. Readers are strongly encouraged to seek advice from qualified legal, financial, tax, and legal professionals before making any decisions related to digital assets or blockchain-based financial systems.